A November Wall Street Journal headline declared, “Companies Grapple with Post-Pandemic Inventories Dilemma.” The first paragraph read, “Companies are wrestling with how big their inventories should be, since the pandemic highlighted the danger of having both too much and too little stored away.” According to the article, the most important inventory question facing managers today is whether their supply chains should be just-in-time (with low inventories) or just-in-case (with high inventories).

Two important principles will enable managers to answer this question today:

- The right amount of inventory for a particular product serving a specific customer depends on the customer’s profitability and the product’s demand pattern (in other words, is demand steady or erratic); and

- The right definition of excellent service is always keeping your promises to your customers, but you don’t have to (and should not) make the same promises to all customers.

In other words, the right answer to the just-in-time vs. just-in-case question is both; companies should run multiple parallel supply chains with the supply chain structure and inventory strategy tailored to the specific customer and product.

In the past, this was impossible to do because companies did not have adequate information on customer profitability and product demand patterns. Instead they had to watch broad aggregate financial metrics like revenue, gross margin, and cost. They also had to monitor aggregate supply chain metrics like the percent of complete on-time order shipments. As a result, service intervals (the time between when an order is received and when the customer receives the shipment) were typically the same for all customers. In that era, it made sense to have broad, companywide policies for inventory management, like just-in-time vs just-in-case.

But today, advance analytics and business intelligence tools, such as an enterprise profit management (EPM) system, can provide profitability metrics down to the transaction level. These systems can produce the profit and demand variance information needed to set the right inventory and service intervals for every product ordered by every customer. Because an EPM system tracks every order, managers can determine both every customer’s demand variance (order pattern) for every product they purchase and every customer’s profitability. This enables astute managers to make the right service interval promises to each customer for each product, which provides the basis for determining the right inventory levels for each customer-product set.

Managers across industries who use EPM systems typically find a characteristic customer profitability pattern:

- 20% of their customers typically generate about 150% of the company’s profits. These “Profit Peak” customers are their large, high-profit accounts. For these customers, the objective is to flawlessly meet their needs and find ways to create service innovations that grow these relationships.

- 30% percent of their customers are large, money-losing accounts that end up eroding about 50% of the profits gained from the “Profit Peak” customers. In our experience, the problem with these “Profit Drain” customers is rarely that they are being offered below-market pricing but rather that they are accruing excessively high operating costs. For example, the customer may be ordering too frequently or holding excessive safety stock. In many cases, these practices are costly for both companies but can often be easily reversed.

- 50% of their customers are small accounts that produce minimal profit but consume about 50% of a company’s resources. For these “Profit Desert” customers, the goal is to reduce the operating costs associated with serving them while growing the few that are development prospects.

When a company is able to identify which of the three profitability categories a customer falls into and what the demand/order pattern for the product is, it finally becomes feasible and practical to tailor its inventory strategy to the customer. The company can now individualize (and keep) its customer service promises.

Make the right promises

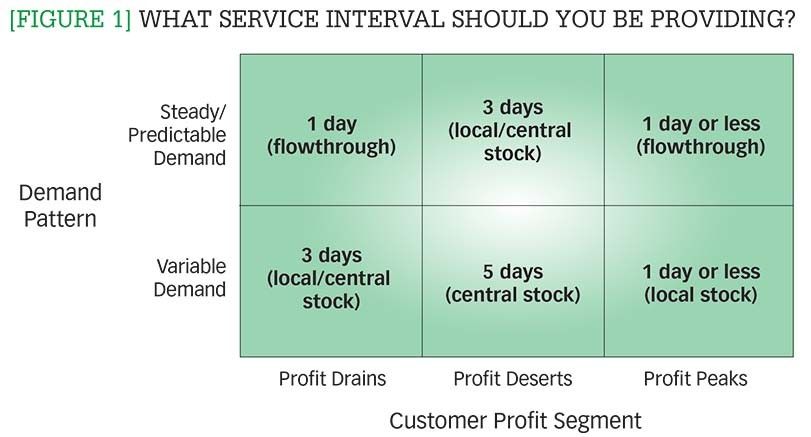

Figure 1 presents a matrix that shows example service intervals that a company might promise to its customers. The columns represent profit-based customer segments, while the rows represent steady- vs. variable-demand patterns.

[Figure 1] What service interval should you be providing?

Enlarge this image

Profit Peak customers and steady-demand products: Your Profit Peak customers provide your core profitability. Your most important supply chain task is to give each profit peak customer what it needs every time (unless supply chain disruptions make this impossible for a time). Their service interval is set at one-day (or less).

The amount of inventory needed for your profit peak customers depends on their demand variance. (Actually, it depends on the degree to which you can forecast their demand; a customer may have a lot of variance, but if you can forecast it, you can plan your inventory purchases to match the customer’s demand peaks and valleys.)

High-profit customers with steady demand products (for example, major urban hospitals buying IV solutions) only require low inventory levels. Their supply chains should be “flow-through pipelines” with minimal inventory at each point. (In other words, inventory should be replenished at a steady rate at every point in the supply chain to match the customer’s steady volume of consumption. You should only hold just enough safety stock inventory to meet emergencies.)

Profit Peak customers with variable-demand products: High-profit customers with variable-demand products (for example, major urban hospitals trying a new type of safety glasses) warrant a lot of safety stock. For these critical customers, you need to carry enough just-in-case inventory to ensure that they will almost never run out of product.

If the local distribution center (DC) runs low on one of these products, you should expedite shipments from a central facility at no cost to the customer. Their service interval is set at one day, as well.

Profit Drain customers with steady-demand products: Profit Drain customers with steady-demand products (for example, distant mid-sized hospitals purchasing IV solutions) also require only low levels of inventory. They also should have flow-through pipeline supply chains. However, their steady demand means that you will not have to carry safety stock locally. If local stock is tight, they should have lower priority than your Profit Peak customers.

Here, the service interval again should be one day, with the understanding that it will stretch to two to three days on the rare occasions that your local DC is low on stock and reserving product for your Profit Peak customers. If they insist on getting faster service in these unusual occasions, they should bear the cost of expediting the product from a central warehouse.

Profit Drain customers with variable-demand products. If a large, money-losing customer has erratic demand for a product (for example, a distantly located mid-sized hospital buying fashionable flowered gowns), it is not necessary to hold high levels of local safety stock. Instead, you should set a service interval (perhaps three days) that enables you to bring stock in from a central warehouse. The safety stock inventories of these products in the local DC should be reserved for your higher priority Profit Peak customers.

Profit Desert customers with steady-demand products: Your Profit Desert segment is comprised of numerous small customers. Typically, the top quartile of this segment (arrayed in descending order by profit) is quite profitable, the bottom quartile is quite unprofitable, and the middle quartiles produce negligible profits. Although the aggregate demand is stable, the demand for a local DC serving these customers can be very unpredictable.

The top quartile Profit Desert customers should get priority on order fulfillment over the other three quartiles. The service interval for steady-demand products (for example, consumables ordered by small machine shops) might be set at three days. In most cases, your top quartile Profit Desert customers will receive their orders in one day, but if your large Profit Peak and Profit Drain customers have a surge in demand, the three-day service interval provides ample time to bring product in from a central warehouse while still meeting your service commitments. The other three quartiles of Profit Desert customers would typically have a three-day service interval.

Profit Desert customers with variable-demand products: The service interval for variable-demand products sold to customers in the Profit Desert segment (for example, a specialized machine tool needed by a small machine shop for an occasional project) might be set at five days. This will provide ample time to bring product in from a central warehouse while giving priority on DC stock to the Profit Peak and Profit Drain customers. Because the majority of products typically have variable demand, this will greatly reduce your overall inventory costs while maintaining your high service levels. If a Profit Desert customer needs a product quickly, it should pay the cost of expediting the product from a central warehouse.

Manage your account relationships

Tailoring your service intervals to match customer profitability and demand pattern will help you keep your inventory low while keeping your service level high. If you don’t tailor your inventory strategy, you risk facing stockouts for your Profit Peak customers or carrying expensive safety stock for the Profit Drain and Profit Desert customers (which is not economically justified). The key is to be clear in advance about the “rules” of how you will serve your customers. If you always keep these promises, your service level will be 100%.

This process might raise concerns that customers will leave for other suppliers with uniformly short service intervals. However, this is often not the case. Most major customers have their own in-house inventories and are simply issuing periodic replenishment orders. Oftentimes if the service interval is a few days, the customer can adequately plan for this. The real reason why most customers want very fast deliveries is that they do not trust the supplier to meet its commitments, and the reason why most suppliers can’t meet their commitments is because they make the same short-interval commitments to every customer. If you keep your service commitments 100% of the time (and accommodate the occasional actual emergency need), your customers will be fully satisfied. If your customers do complain about your service intervals, they have the option of working with you to bring your return on serving them up to a level that warrants a shorter service interval.

Moreover, the differentiated process described above commits to one-day (or less) service intervals for all Profit Peak customers on all products and even for Profit Drain customers’ steady products. Most Profit Drain customers can tolerate a short wait for variable-demand products, especially for periodic restocking orders. Your Profit Drain and Profit Desert customers should pay compensatory prices if they want uniformly quick service and not require you to make your Profit Peak customers cross-subsidize the losses that they cause.

Manage your supply chain(s)

This process of carrying the right inventory for each customer segment is very manageable. We have described only six business segments: Profit Peak customers, Profit Drain customers, and Profit Desert customers—each with ether steady or erratic demand.

In complex companies, this matrix can be expanded to address more customer segments (for example, special development accounts) and product types (for example, mission-critical parts). However, increasing the complexity quickly makes the system much more difficult to manage and maintain.

By tailoring their inventory strategy to the customer-profit segment, managers can boost their profitability by providing the right set of incentives for each segment:

- Profit Peak customers get consistently fast service, with constant priority on inventory;

- Profit Drain customers get appropriate service promises, which are always kept, and they have an incentive to engage with you to bring your profitability on serving them to Profit Peak levels (giving them priority on inventory);

- Profit Desert customers get appropriate service promises, which they can rely on, and they have an incentive to grow their business and profitability to Profit Peak status.

This practical process enables you to define multiple parallel supply chains, each appropriate for a distinct business segment. This is the key to setting the right inventory level for each product, aligning them with your changing business, and using your supply chain to fuel your profitable growth.