COVID-19 has hit supply chains with a “double whammy.” It’s not just that supply of vital medical equipment, pharmaceuticals, and essential consumer staples has crashed. Companies have also seen a plunge in demand as more than 30 million workers lost their jobs and shelter-in-place rules halted normal commerce. Meanwhile the already booming e-commerce sector has kicked into overdrive.

How will these large and rapid changes impact the distribution warehousing sector here in the United States? From my vantage point as a corporate site selection consultant, I have identified some of the key trends that I see having an impact on site locations and design decisions.

Move toward reshoring

Reshoring of manufacturing and supply chain operations from China back to the U.S. has been a trend since the Trump tax cuts, but we expect the pace of this supply chain realignment to pick up even more now. The pandemic has brought into the spotlight the fact that our nation’s supply chains have been stretched to the limit at our great peril. COVID-19 has been a painful wakeup call that our supply chains—normally hidden from public view—are far too reliant on distant nations like China. The message of supply chain risk has even reached the halls of the U.S. Congress where lawmakers—on both sides of the aisle—are crafting legislation to encourage American companies to shift supply chain operations from China back to the U.S. through the use of tax breaks, generous subsidies, and new rules of the road.

As a result, we expect that warehouse site selection within the U.S. will become less “port centric” and more oriented to the dynamics of domestic production and consumption. In recent years, some of the most popular and expensive supply chain real estate has been close to deep-water container ports like Miami, Florida; New York/New Jersey; Southern California; and Houston, Texas. We see that interest moderating and predict a heightened interest in warehouse sites near centers of U.S. manufacturing and agricultural production, especially in our nation’s central region.

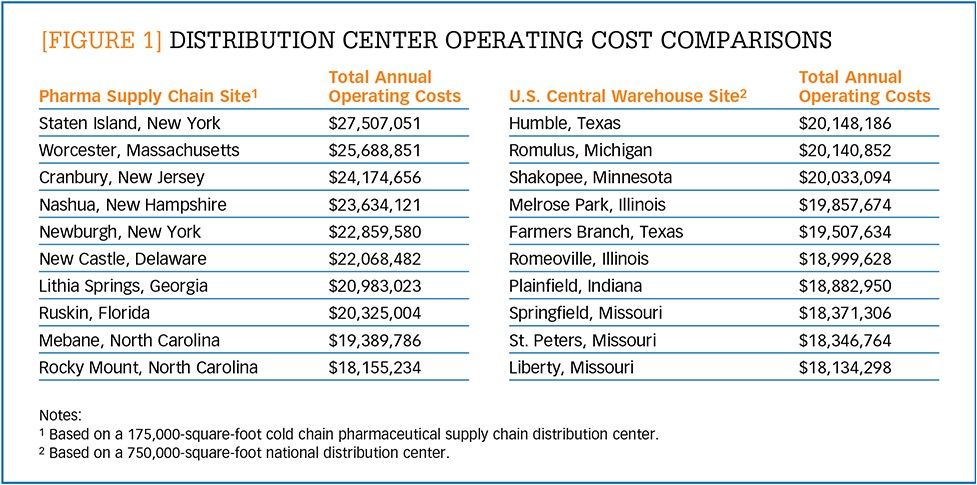

Weakened economy

Interest in keeping a close eye on cost efficiencies and operating costs will intensify in the weakened COVID-19 economy. As a result, companies may favor lower-cost cities and states with more favorable tax regimes for their supply chain facilities. Figure 1 lists ten top locations on the U.S. East Coast for a cold chain distribution center serving the pharmaceutical industry and shows the comparative operating costs (labor, real estate, construction, power, taxes, and shipping) for a 175,000-square-foot facility. Annual costs range from a high of $27.5 million in Staten Island, New York, to a low of $18.1 million in Rocky Mount, North Carolina. The cost differential between the New York location (a state with a corporate income tax rate of 6.5%) and North Carolina (a state with the nation’s lowest corporate income tax rate at 2.5%) is $9.4 million, a significant differential of 34.2%.

Enlarge this image

Also shown in Figure 1 are ten top Central U.S. DC sites along with annual operating costs for a 750,000-square-foot national warehouse. Annual costs range from a high of $20.1 million in Humble, Texas, to a low of $18.1 million in Liberty, Missouri. Three of the ten top national DC sites are in Missouri which records the lowest corporate income tax rate in the Central U.S. and the second lowest in the nation at 4.0%.

Site-seeking companies need to be on guard for major tax hikes and toll increases in the months ahead. Those states hardest hit by COVID-19 will face unprecedented budget challenges and will be searching for new revenue sources. California, for example, is gearing up for a large property-tax hike. The state’s November ballot initiative would effectively exclude commercial and industrial properties from the landmark Proposition 13 passed in 1978 that limited property taxes for homes, businesses, and all other land to 1% of the property's value at the time it was last sold. If passed, this game-changing initiative is expected to hike property taxes for California businesses by as much as $12 billion.

At the same time, the weakened economy may also open up new sources for distribution sites. Some of the nation’s most attractive commercial real estate will be the many millions of square feet of retail space that will not be coming back after COVID-19. Developers will be especially quick to repurpose former malls and “big box” stores. These sites may prove attractive to developers due to their low cost, highway access, and truck and employee parking accommodations.

The role of risk management

Conventional risk management has always been part of the warehousing location decision. Companies have long taken into account such considerations as the integrity of the physical site, insulation from natural disasters, and political stability when choosing where to locate a warehouse or distribution center. The pandemic, however, will greatly expand the boundaries of risk management and its role in site selection. It will now need to include a range of COVID-related considerations like transitioning to new suppliers and/or customers as well as transitioning away from some that may go out of business due to COVID. Similarly, DC design and management will need to consider a myriad of human resourcefactors related to the impact of the virus on the DC’s workforce and local labor market as a whole.

Rising importance of the cold chain

COVID-19 will change not only where warehouses and DCs are located but also how they are designed. Cold storage was already on track to become a much larger player in the supply chain before COVID-19. Now, we are seeing unprecedented interest in the cold chain from investors and site-seeking industries like pharmaceutical and food. Our firm’s BizCosts unit forecasts that between 100 million and 125 million square feet of freezer/cooler space will be required to meet new demands, much of it coming from pharmaceutical, biotech, and food processing companies.

This trend is expected to continue beyond COVD-19. We expect to see many consumers continue to order perishables, including frozen food, online. Additionally, pharmaceutical and biotechnology firms are developing a wide range of new products that rely on cold storage throughout the entire supply chain. Biologics—drugs and medicines developed from living organisms—are also driving new cold storage demands. The cold chain will become even more critical when the much anticipated COVID-19 vaccine is developed, and the pharmaceutical supply chain has to handle distribution of an unprecedented number of dosages.

Technology and connectivity

COVID-19 is also causing a spike in warehouse automation. Some companies are turning to robots to help maintain social distancing and keep workers safe within the warehouse setting. Fetch Robotics, a provider of warehouse robotics, reported that inquiries are up by two-thirds since the emergence of COVID-19. Walmart says that concerns about worker safety are driving its dealings with Bossa Nova Robotics, which is designing a new shelf-scanning robot for the mega-retailer’s warehouses and stores.

Greater use of robotics will also be encouraged by the COVID-19-driven reshoring of manufacturing and supply chain facilities back to the U.S. This type of automation will help companies offset higher U.S. operating costs, principally in the area of labor.

COVID-19 has also accelerated the trend toward remote working, which will have a significant impact on the U.S. commercial real estate industry. As more employees work from home, the demand for office space decreases. When we started our firm in the 1970s, many U.S. offices averaged 500 square feet per worker. That number dropped down to 200 square feet per worker a decade ago and is now less than 150 square feet per worker. For warehousing projects, we expect to see less space allocated to other back office functions (such as accounting, sales, and customers service) that may be co-located at the site.

Rewriting the script

It’s important to remember that no one saw this coming. There’s been no script for supply chain players to follow when it comes to reacting to and dealing with the COVID-19 pandemic. Instead supply chain companies and their consultants have been writing a new script each and every day.

Given the industry’s ability to adapt quickly to changes, I have no doubt we will recover from this horrible event with a more secure and resilient supply chain in tune with the “new normal.” … What that “new normal” is, however, still remains to be determined.