The past four months have been unprecedented in the supply chain world—an understatement you might say! It’s not just that the ongoing global pandemic has laid bare the complexities and vulnerabilities of modern supply chains. There has also been unprecedented media attention paid to supply chain management. For better or worse, now the whole world knows about supply chains. In particular, warehousing and distribution have been brought out of the shadows and into the bright media lights for the critical role they play.

The upcoming edition of the “Logistics 2030” (L-2030) report, sponsored by JLL and CenterPoint, will focus on the growing importance of warehousing and distribution and the strategic direction they will take over the next decade. The annual study is conducted by the Center for Supply Chain Innovation at Auburn University in partnership with the Council of Supply Chain Management Professionals (CSCMP), the National Shippers Strategic Transportation Council (NASSTRAC), and AGiLE Business Media (publisher of DC Velocity and CSCMP’s Supply Chain Quarterly). This year’s report is based on multiple in-depth focus group discussions with leading supply chain executives and survey responses from a wide range of supply chain professionals. The release of the Logistics 2030 warehousing report and a related panel discussion are scheduled for August 20 at the fourth annual Fusion 20/20 Supply Chain Symposium (www.auburnscm.org/events).

The focus group meetings and survey results highlighted a key point: Even before the onset of COVID-19, the role of warehousing and distribution had been in transition from supporting downstream supply chain functions to operating as a frontline service provider to end customers.

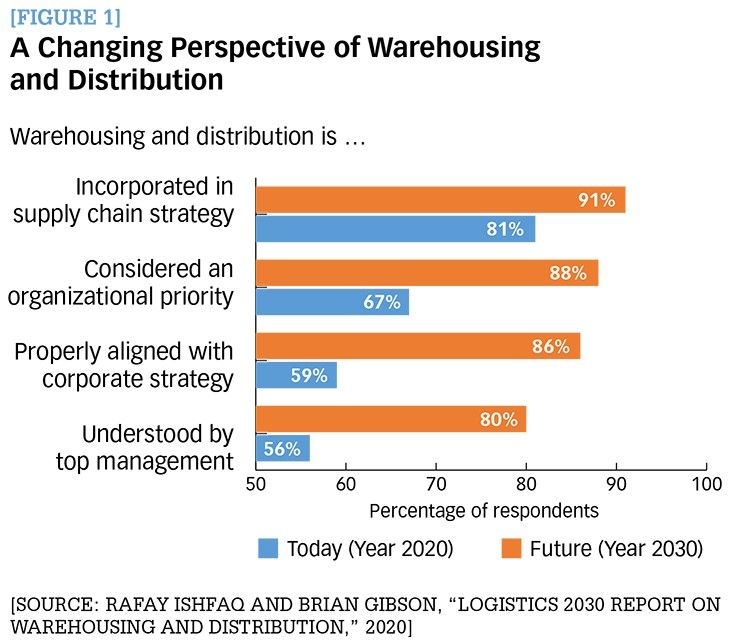

This is quite a turn of events. Historically, warehousing and distribution were considered a cost center by business executives—a function that needed to be economized. But this view is now changing. A large majority (80%) of survey respondents in our L-2030 study point to a shift in the way top management in their firms think about warehousing and distribution. They are now recognizing the business value warehousing and distribution can provide. We notice a near consensus among survey respondents (88% agree) that warehousing and distribution will be an organizational priority by 2030. (See Figure 1.)

Enlarge this image

The shift is on

A key trend underlying the new value proposition for warehousing is the ongoing shift in the supply chain structure. Supply chain executives in our focus groups point to the decentralization of supply chains arising from the need to push inventory closer to the customers. As one respondent said, “We’re going to be relocating facilities closer to customers in response to the need for faster deliveries. We’re going to put facilities in multiple places as opposed to just being at the most geographically central place.” Survey results indicate that firms’ push for forward inventory placement will continue into the next decade. The use of retail stores to fulfill e-commerce orders is expected to double. Additionally, 68% of respondents expect to see an increase in the use of local fulfillment centers and a 51% increase in regional distribution facilities by 2030.

Developing a decentralized warehousing and distribution structure requires major investments in infrastructure and technology. A big part of these future investments will be targeted towards expanding firms’ distribution networks. Eight-five percent of survey respondents expects a significant increase in corporate funding to improve warehouse and distribution. These investments will go towards developing key capabilities deemed essential in the coming decade: expanding distribution networks (71% of survey respondents agree), incorporating flexibility in capacity and warehousing operations (68%), leveraging automation for speed (62%), and cutting distribution costs (61%).

Our discussions with focus group executives highlighted a key capability deemed critical in the coming decade – flexibility in adjusting warehousing and distribution capacity. The importance of this capability is rooted in the need to respond to the ever-shifting whims of customers, now and in the future. Firms are investigating ways to be nimble by adjusting their supply chain capacity to match the continually changing demand patterns. “We’re looking at logistics facilities that are flexible in size, construction, and attributes geared towards a cross-dock-like capacity,” explained one respondent Thereby, a necessary capability in warehousing and distribution would be the agility to expand (and shrink) capacity quickly.

Embrace the tech

We asked focus group executives and survey participants how they planned to implement their decentralized distribution strategy. A clear consensus (supported by 93% of survey respondents) is that firms are looking to leverage technology as a catalyst to upgrade their warehousing and distribution processes.

In our study, we noticed a clear change in the conversation around technology that went beyond the typical issues of acquisition costs and implementation pains. We found supply chain executives to be focused more on a broader return on investment (ROI) perspective. One executive highlighted this point as follows: “We know that warehouse labor isn’t going to get any easier to recruit or retain. So as soon as we can justify ROI to replace labor with technology, we’re ready ‘to swing the bat’.”

Another element of this new conversation is the need for execution speed. One executive articulated this point as follows: “So in our [distribution centers] (DCs) we’re investing in ways to unload faster [and] load faster to make fulfillment of things faster so that we can do more with less people.” The cost-benefit analysis for technology solutions is starting to tilt towards a favorable business case for early adoption. “The economics of technology and what you consider in terms of labor availability and how far you’re willing to think about cost escalation or things like healthcare and fringe benefits. I think it’s changed the game in terms of the business ROI,” said one executive.

Our survey results indicate a high use of order management system by 2030 (71% of respondents agree). This software would align inventory and customer orders for fulfillment and shipping across multiple channels. Another big increase is expected in the use of warehouse execution systems (from 16% currently to 61% in 2030) that can provide a real-time coordination of labor and equipment for automated picking, packing, and shipping. Based on the survey results, we project that more firms will start using traditional warehouse management systems (an increase of 67%) by 2030.

In response to our survey question about technologies that have the most potential to disrupt warehousing and distribution, supply chain professionals identified the following: predictive and prescriptive analytics, automated guided vehicles, automated storage and retrieval systems, and automated conveyor systems. It is interesting to note how these technology choices align with automation, capacity expansion, and speed of distribution; all of which support operationalizing the emerging decentralized supply chain structure mentioned above.

In conclusion, warehousing and distribution are marching forward towards fulfilling their new role of a frontline function that drives business growth for firms. As the pendulum swings back to a decentralized supply chain structure, we expect companies to increasingly implement technology in warehousing and distribution in the coming years. To develop the necessary capabilities of speed and flexibility, supply chain executives are strategizing to make the requisite investments in distribution networks, incorporate technology, and engage capable third-party logistics partners to harness the opportunities that lie ahead.

[Authors’ Note: The Auburn University Fusion 20/20 Supply Chain Symposium will be held on August 20th. Register at www.auburnscm.org/events]