This year’s annual “State of Logistics Report,” released today by the Council of Supply Chain Management Professionals (CSCMP), comes at a time when many businesses are reevaluating their logistics and supply chain strategies in the face of the Covid-19 pandemic and its related economic effects. As such, the report seeks to pause and provide a big picture view of the past year as well as some perspective on the path forward.

Now in its 31st year, the “State of Logistics Report” is researched and prepared by the consulting firm Kearney and sponsored by Penske Logistics. The report seeks to provide an in-depth look at the logistics industry, most notably by calculating U.S. business logistics costs as a percentage of gross domestic product (GDP) and pointing out major trends.

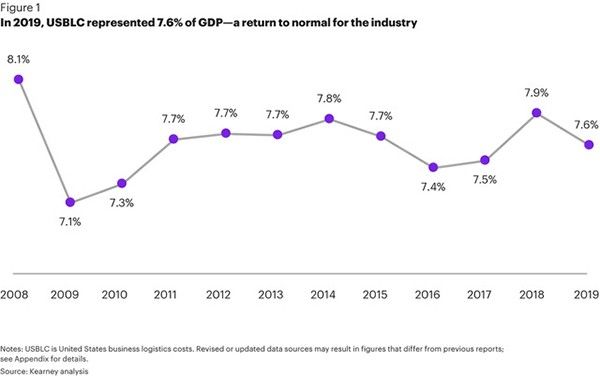

According to the report, logistics expenditure rose to $1.652 trillion in 2019 or 7.6% of the U.S.’s GDP of $21.4 trillion. This represented an improvement over 2018, when costs were at 7.9 percent of GDP. Indeed, 2019 felt like “a return to normal” after a “torrid” 2018, which saw increased logistics costs due to fast GPD growth and capacity shortages, according to the report.

Enlarge this image

However, that normal ran smack into an unprecedented pandemic, which led to measures such as social distancing and business closures. These efforts have derailed the economy and plunged the country into a recession. As the report’s introduction states, “The pandemic and global measures taken to reduce its further spread have decimated supply chains, scrambled logistics capabilities, and destroyed huge swaths of demand.”

The effects of the pandemic on the different logistics modes and nodes have been variable and unpredictable according to the report. For example:

- Motor freight: Profitability was already suffering for motor carriers in 2019 as slowing demand and increased capacity led to a drop in freight rates and a rise in bankruptcies, even before the pandemic. This year, the report writers expect that small carriers with a small list of clients in the most affected industries (such as automotive, hospitality, and durable goods) will be the hardest hit by the pandemic. Large carriers will need to use technology to optimize asset utilization and routes to help them navigate the storm. Meanwhile, smaller carriers will need to turn to app-based solutions and brokers.

- Parcel: Meanwhile the pandemic has been “a shot of adrenaline” to the parcel sector, as consumers turned to e-commerce and home delivery in the wake of the shutdown of physical stores, according to Zimmerman. Even before the pandemic, the parcel sector was growing strongly, with costs rising 8.5% in 2019.

- Rail: The Covid-19 pandemic hit the rail industry hard, as it came out of 2019 with improved operations but declining volumes. The pandemic has caused a volume to drop even further, with year-over-year traffic down 25 percent.

- Air: In 2019, the air freight sector saw costs fall by 9.7 percent, as the economy slowed down and volumes decreased. The pandemic led to a sharp decrease in air passenger travel, which in turn cut into cargo capacity, causing spot rates to soar.

- Ocean: In response to the Covid-19 outbreak, ocean shipping companies cancelled sailings, reduced capacity, and raised rates. Volumes could rise in the second half of 2020 as Asian plants catch up to their backlog of demand, according to the report. However, carriers were already dealing with overcapacity and some may have to merge.

- Warehousing: Rising e-commerce sales have continued to feed the demand for warehousing space. According to Zimmerman, new warehousing capacity was snapped up as quickly as it came online. This sentiment was echoed by Mark Althen, president of Penske Logistics during the panel discussion following the State of Logistics press conference. “We’re seeing increased activity in warehousing,” Althen said. “Shippers are looking to increase storage capacity closer to customers. They’re starting to move away from larger centrally located [distribution centers] to ones closer to urban areas.

THE WAY FORWARD

Many economists are tentatively predicting an economic rebound to begin in 2021. But according to Zimmerman, “the size, shape, and timing of the recovery remain in question.” Furthermore, for that recovery to happen, companies will need to quickly adapt and change their logistics abilities. Both the report and the panel discussion following the press conference outlined some of the changes that might occur. These included:

- A move away from single sourcing toward “multi-shoring,” where companies rely on suppliers located in different countries and regions. According to Zimmerman, many companies had already started to make this major strategic shift as trade tensions began to rise in 2018. “Many of [Kearney’s] clients are diversifying away from China toward other low-cost countries and even the U.S. so that they have more options in their supply chain,” he said.

- A similar move away from just-in-time fulfillment and lean inventories to larger inventories and more reserve capacity, as companies seek to increase the resiliency of their supply chains.

- Greater demand from shippers for increased flexibility in how warehousing and third-party logistics companies manage their inventory and storage space. One option is taking a campus approach, where customers are housed in one location, said Zimmerman.

- Risk and resiliency will become as important a consideration in supply chain design as speed and efficiency, and companies will employ more risk analysis in choosing supply chain partners.

- Increased reliance on technology. According to Zimmerman, one of the reasons why logistics costs dropped in 2019 was that more transportation companies were using technology to optimize asset utilization and routes. To emerge from the current crisis, companies will need to continue to make investments in effective technology, including warehouse automation, machine learning, and artificial intelligence.

In spite of the immense challenges that transportation and logistics companies have faced these past three months, the report asserts that the industry’s prospects are brighter than other sectors of the domestic economy. Zimmerman and his co-authors maintain a hopeful position that logistics is “an industry initially traumatized but ultimately resilient.”