Recently the supply chain landscape has been flooded by a massive wave of new technologies and associated strategies, leaving practitioners with the daunting task of sorting out which ones are right for them.

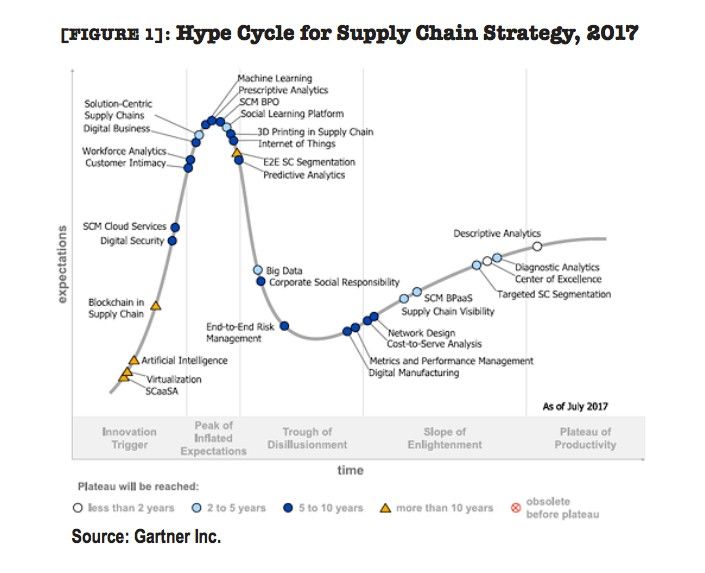

To help ease that pain, Gartner Inc. recently released its "Hype Cycle for Supply Chain Strategy, 2017," which graphically shows where various technologies and technology-enabled strategies lie along the adoption curve. (To see the cycle and read an explanation of the methodology, see the associated sidebar, "Gartner's Hype Cycle explained.") In particular, the report highlights nine that it says will achieve mainstream adoption levels in five years or less:

1. Descriptive analytics is the application of analytics to describe what is happening or has happened. It includes such capabilities as reporting, dashboards, supply chain visibility, data visualization, and alerts. According to Gartner, many organizations report that descriptive analytics have already helped to significantly improve their operations. Indeed this is the only technology covered in the report that Gartner believes has matured enough that its applicability and relevance are well understood and the criteria for evaluating a vendor are clearly defined.

Estimated time to mainstream adoption: less than two years

2. Centers of excellence (COEs) are centralized groups that focus on identifying, designing, developing, and implementing best practices across the business. Gartner's research indicates that 78 percent of supply chain organizations have one or more COEs. However, many of these COEs lack a coherent organizational structure, says Gartner, due to weak mandates, uncertain missions, and unclear governance and performance metrics. For this reason, Gartner does not believe that the practice is fully mature. However, as more organizations advance their expertise, Gartner expects the COE will develop further and be used more productively by more companies.

Estimated time to mainstream adoption: within the next two years

3. Diagnostic analytics seek to explain why something—an event or a trend—happened. According to Gartner, to implement diagnostic analytics, a company needs to have already implemented descriptive analytics and have a clear understanding of all the relationships in its supply chain. As analytics in general improve and the availability of real-time data from technologies like the Internet of Things (IoT) increases, Gartner believes that more companies will implement diagnostic solutions.

Estimated time to mainstream adoption: two to five years

4. Targeted supply chain segmentation involves techniques such as categorizing customers or suppliers as high priority or treating parts or inventory differently based on volume. While segmentation has been around as a concept for at least 10 years, a documented approach based on industry consensus will go a long way toward speeding up adoption.

Estimated time to mainstream adoption: within the next five years.

5. Supply chain management business-process-as-a-service is an external service that delivers standardized processes through a cloud-sourced technology platform. Examples include compliance and regulatory reporting, freight forwarding, customs processing, and aftermarket services. These services allow companies to gain incremental capabilities and efficiencies without having to buy a new software license or hire new employees.

Estimated time to mainstream adoption: two to five years.

6. Supply chain visibility involves generating timely, accurate, and complete views of plans, events, and data across the entire supply chain, including external partners. Many organizations currently lack an end-to-end approach to supply chain visibility, says Gartner. But the firm believes that such visibility will become more standard as more mature IoT technologies and analytics solutions become available.

Estimated time to mainstream adoption: over the next two to five years

7. Big data technologies are used to analyze large datasets to reveal patterns, trends, or associations. According to Gartner, there is a now a "post-hype" realization that more data does not necessarily lead to better insights. Today, organizations are focusing on improving analytics and integration to get more out of their big data.

Estimated time to mainstream adoption: another two to five years

8. Social learning platforms provide personal productively tools, Web 2.0 applications, content repositories, and data sources that can help employees learn and share knowledge. In the supply chain space, Gartner sees social learning platforms as one way to address the large number of long-term employees retiring. They allow companies to capture their knowledge and share it with younger workers in a way that can be scaled across multiple business units and geographies. Gartner recommends integrating social learning within the company's organization-wide information technology (IT) program.

Estimated time to mainstream adoption: two to five years

9. Solution-centric supply chains offer customers a personalized collection of products, data, and services from a digitally enabled ecosystem of partners. It's an approach seen mainly in the high-tech, medical, consumer, and industrial sectors at the current time.

Estimated time to mainstream adoption: five years

All of these strategies and technologies are indicative of a general trend toward the "digitalization" of the supply chains, says Noha Tohamy, Gartner's vice president of supply chain research.

"Looking further out than five years, we can expect even more exciting technologies coming over the horizon," said Tohamy. "We expect that artificial intelligence, machine learning, corporate social responsibility, and cost-to-serve analytics will all drive significant shifts in supply chain strategies within the next decade."